The price of property is always claimed to be set by a "market". In reality, a nation's property prices can be deliberately moved by changing tax laws, by restricting land and infrastructure supply, by repressing interest rates and changing lending rules. In reality, there are plentiful ways to manipulate property prices, that have nothing to do with "markets" or supply and demand for a place to live. In Australia, a prime example is the tax deductibility of losses incurred on so-called investment properties, in effect a government subsidy to property speculation. These are deliberate policies to ramp property prices, put into effect by political majority, creating a bubble economy that gradually has come to engulf other actually productive areas of society. As financials make up an increasing proportion of the economy, with more people and time spent, this constitutes an enormous drag on the actually productive.

The valuation of property is also surprisingly simple, and as always comes down to cashflows. Since the long term cashflows of property are much more stable than those of shares, calculating the fair value of property is in fact easier than valuing most shares. In the long term, average net rental cashflows follows average income closely, and in the very long term both are expected to converge with inflation. Just as the value of a stock is the sum of all future dividends discounted at an appropriate risk-adjusted rate, so the value of property is the sum of all future net rental cashflows discounted appropriately. Property value is thus equal to starting net rental cashflow, divided by the discount rate less the expected growth rate in net rental cashflows.

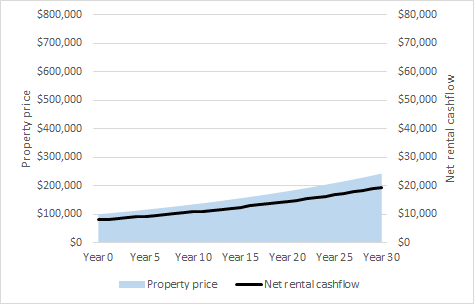

The rent that is or could be charged on a property, less all expenses and maintenance, is what determines value. Increases in the fair value of property can only be driven by a matching expected increase in net rental cashflows, any increase in price beyond that is a burgeoning bubble. Assume a model where the average property price at Year 0 is $100,000 and the net rental cashflow is 8,000, with both prices and net rental cashflows increasing by 3% annually. Over 30 years, price increases to $242K and net rental cashflow increases to $19K, with net rental yields constant at 8%.

In this model economy at equilibrium, long term property price growth equals long term net rental cashflow increase. (The model assumes constant increases each year purely for presentational ease, the conclusions are independent of this assumption. Also, note that a long term model of property prices need not include variations to the central bank interest rate, since in the long term the sum of central bank rate movements is zero.) But 3% capital gains are no fun and generate no bankster bonuses, no boom times or popping champagne corks, just boring sustainable growth. Assume instead that a political majority aided by banksters, a stealing generation if you will, decide to implement policies to deliberately inflate the price of property at a 7% growth rate. This growth is of course financed by debt, aka money created out of thin air.

In this scenario, net rental cashflows and the fair value of property remains the same, but property prices rise to $761K in Year 30, sending net rental yield down to 2.6%. Anyone buying property in Year 30 is paying $242K for the actual property, and a further $518K for a ticket to the state sponsored pyramid scheme that has been created. In Year 30, two thirds of property prices constitute a down payment to the government sponsored pyramid scheme. The only reason anyone is willing to pay $761K in Year 30, after years of unsustainable increases in price, is the expectation of further increases. In time and with enough "benevolent" intervention, future expected price increases become priced into the market, and the bubble fuels itself.

This is most clear in Australia, with more than 50% of house purchases going to property "investors" (actually leveraged speculators on the government sponsored pyramid scheme). The majority of these property "investors" incur running losses on their "investment", and are thus without question making the purchase based on expected future capital gains. This is an acknowledged fact. Meanwhile the presstitutes and analysts tie themselves into knots trying to explain why this is not at all a textbook bubble, when an asset is bought solely on the expectation of further rises. The latest explanation is the most humourous: it is not a bubble because Australia has many "coastal cities". Such a non sequitur could only pass as intelligent comment in an idiocracy, it proves not only the idiocy of the commenter but also the stupidity of the society that promotes said commenter to a position of power.

But how can bubble economists admit that lowering rates and changing tax laws boost asset prices, yet simultaneously claim prices are set by an efficient market? This is solved by circular thinking and the so-called wealth effect. Bubble economists believe that if we ramp up asset prices by lowering rates, the higher prices will inexorably lead to higher economic activity (the wealth effect), with the fair value of this increased economic activity perfectly matching and justifying the increased asset price. So if we ramp shares/property, this increases future cashflows for shares/property, so that the initial ramp was just a fair value movement by an efficient market. The initial manipulation of the market was therefore not manipulation. Because of efficient markets and the wealth effect, markets are essentially non-manipulable, therefore we should manipulate them as high as possible (this power should of course be yielded to only the most prudent and benevolent central bank bubbleheads). This is not meant as parody, this is what bubble economists actually profess to believe. If their premise were correct, i.e. if markets with absolute certainty always were and always will be perfectly efficient, their logic would be flawless. If you knew a car's speed gauge was perfectly correlated with vehicle speed, and could not for any reason ever be incorrect, it would make sense to try and move the car by pushing on the speed gauge with your finger.

Both political parties, all "respected" economists and every mainstream economic journalist fully support the bubble economy that western democracies have descended into. To challenge the bubble paradigm is to invite ridicule and revulsion. In Australian media it is forbidden to say that we have a bubble, likewise the bubblehead of the Reserve Bank and other banksters would never admit there is a bubble, regardless how grotesquely prices become detached from reality and cashflows. (At most they are permitted to say there is maybe a risk of future overheating.) Realistically, 2007 was the point of no return, the time when the west could have abandoned the bubble economy and dismantled the expanding beast of finance and debt-fuelled asset bubbles, but instead decided to inflate an even bigger bubble to cover up the losses that would have been necessary to face, if true price discovery had prevailed. The bubble has gone so far now that no politician could ever propose dismantling it. The campaign slogan "I'll crash house prices! (But it's necessary for our future)" is not likely to be popular.